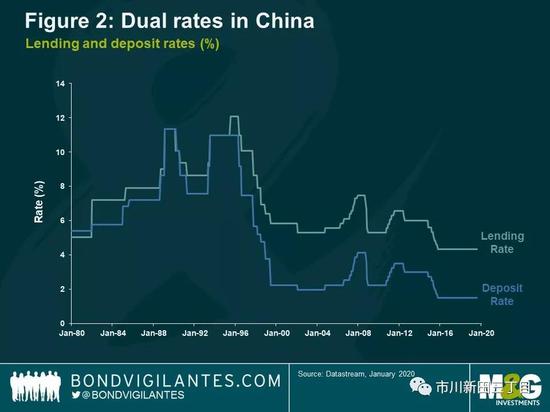

Interest rates on deposits and loans were set independently. When stimulus was required, interest rates on loans could be reduced by more than interest on deposits. In an economy with fiat money, nominal spending can always be stimulated.

图2显示,当时中国的存款和贷款利率被设置在不同的水平上。当需要加大刺激力度的时候,贷款利率的调降幅度会大于存款利率的降幅。在一个采用法定货币的经济体中,如果出现上述情况,那么名义上的开支总量会加速增长。

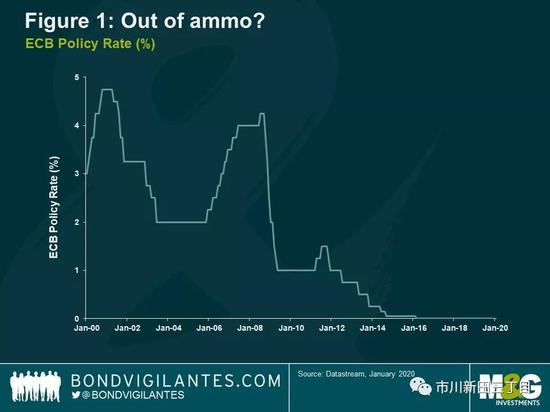

Can such a policy work with a private banking system and an independent central bank? Many commentators seem unaware that in his final act as president, Mario Draghi showed precisely how it is done.

这样的政策在一个由私营的商业银行加独立的中央银行组成的银行体系中会奏效吗?很多评论家似乎并不了解的情况是,欧洲央行前任总裁德拉吉在其任期的最后日子里已经精准地展示出利率双轨制是如何实行的。

For some time now the ECB has had a method of independently affecting lending rates. Its targeted longer-term refinancing operation — or TLTRO — allows the central bank to lend to commercial banks at negative interest rates, on condition that they extend new loans to the private sector. TLTROs also exclude lending to unproductive parts of the economy, such as mortgages.

在经过了一段时间后的今天,欧洲央行发展出了一套做法可以独立地影响借款利率的水平。该行可以通过“定向长期再融资操作”TLTRO以负利率的水平贷款给商业银行,前提是商业银行必须将获得贷款资金转贷给私营企业。欧洲央行还规定“定向长期再融资操作”项下的资金不得用于非生产性用途,比如用于按揭贷款。

Mr Draghi’s final innovation was to introduce “tiered reserves”. This allows the central bank to set the rate of interest on the deposits that banks hold with the central bank independently of the policy rate which determines money market rates.

德拉吉在任期间最后一项创举是引进了“分层存款准备金”制度。该制度可以让中央银行在决定了货币市场利率水平高低的政策性利率之外,为商业银行存放在央行的准备金存款另行设定单独的利率水平。

In one subtle gesture, the ECB in effect reduced the interest rate at which banks can fund lending to the economy and raised the average interest rate that banks receive on their deposits. This is a policy of dual interest rates.

欧洲央行以一种微妙的姿态实质性地降低了商业银行向实体经济提供贷款的资金成本并提升了商业银行在央行存款的利率。这就是利率双轨制政策的实质。

Dual interest rates in the future

未来的利率双轨制

Let us consider how this policy could be extended. If Ms Lagarde needs to provide further stimulus to the eurozone due to inflation persistently undershooting the ECB’s close to 2 per cent target, she could increase the term of TLTROs to five or 10 years, at a steeply negative interest rate, say minus 1 per cent. At the same time, the bank could increase the interest rate on deposits through tiering.

先来讨论一下该政策如何才能推行下去。如果拉扎德因欧元区的通胀增速持续低于欧洲央行设定的2%目标值而需要进一步刺激欧元区的经济,她可能会将“定向长期再融资操作”项下的贷款期限扩大至5到10年期,贷款利率的水平进入更深的负利率区间,比如-1%,同时该行还可以通过“存款分层”的方式提升存款利率的水平。

Progress could also be made on how to target this TLTRO funding. Currently, the only requirement for banks to access the programme is that they use it to extend new loans, excluding mortgages. Ms Lagarde has expressed a desire to make ECB policy consistent with the eurozone policy on climate change.

定向长期再融资操作项下融资的用途也应予以明确。当前商业银行获得“定向长期再融资操作”项下资金的唯一前提条件是将该笔资金用于新发放按揭贷款用途之外的贷款。拉扎德曾表示希望让欧洲央行的货币政策与欧元区在气候变化方面的政策步调一致。

TLTROs at negative interest rates should be available only to banks that are directly using the funds to finance sustainable energy investments. In one relatively simple policy move, the supposed impotence of monetary policy becomes an enhanced Green Deal.

“定向长期再融资操作”项下的负利率贷款应只用于为可持续的能源投资项目提供融资。只经过一个相对比较简单的政策变化,货币政策的“无能为力”就会转变成一个加强版的绿色协议。

It came as little surprise that the take-up of the recent programme was muted. For example, the current three-year TLTROs at minus 0.5 per cent are only a marginal improvement on available market-based funding. But a 10-year loan at minus 1 per cent or minus 2 per cent would be game-changing.

近期“定向长期再融资操作”之所以接受度不高是可以理解的。举个例子,当前三年期“定向长期再融资操作”的融资利率水平为-0.5%,相对于市场融资利率的水平来讲只是略有改善而已,但如果十年期“定向长期再融资操作”的融资利率水平是-1%或-2%,就会产生重大影响。

Dual interest rates and sustainable TLTROs should be at the heart of Ms Lagarde’s review. Monetary policy is very far from running its course. There is scope for a major shift in its power. Therein lies the challenge for the bank’s new president. She has promised openness and transparency. Being explicit about the effects, and powers, of this policy would be a great manner in which to begin.

利率双轨制和可持续的“定向长期再融资操作”应该是拉扎德政策审议的重点。货币政策远非顺其自然那么简单,失之毫厘往往谬以千里。这是摆在欧洲央行新总裁面前的挑战,拉扎德曾承诺要让政策更具开放性和透明性。讲清楚这一政策的效果方才是一个好的开端。

免责声明:自媒体综合提供的内容均源自自媒体,版权归原作者所有,转载请联系原作者并获许可。文章观点仅代表作者本人,不代表新浪立场。若内容涉及投资建议,仅供参考勿作为投资依据。投资有风险,入市需谨慎。

责任编辑:郭建